HMRC HELPS UK BUSINESSES INVEST IN EQUIPMENT BY SETTING THE ANNUAL INVESTMENT ALLOWANCE TO £1M

Why it’s easier to plan spending this year

UK governments have always allowed businesses to reduce their tax bills by investing in capital equipment.

As long as businesses make a profit, they pay either income tax (unincorporated businesses), or corporation tax (limited companies). Tax liability is calculated as a percentage of pre-tax profits.

Capital expenditure: the time is now

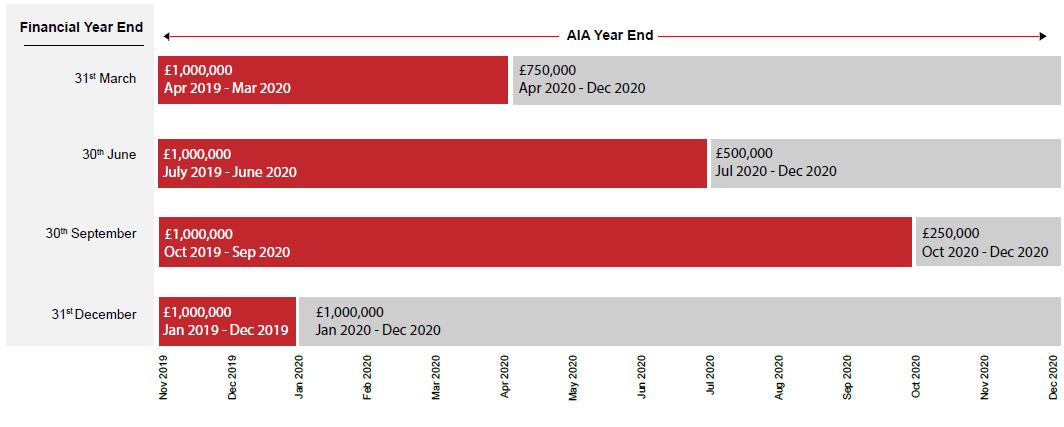

The Annual Investment Allowance (AIA) of £1m has been set for 2019 and 2020. This is the highest allowance set by the government since being introduced in 2008.

This means you can buy qualifying business assets up to £1m, and offset the whole cost against tax for 2019 and 2020 calendar year.

With the changes in allowance you will be required to calculate your entitlement for the fiscal year end. Use the chart below to help.*

*Where your accounting period overlaps you will need to take into account AIA set for that time period.

AIA: rules to consider before you invest

To maximise tax relief on any capital investment, make sure you’re aware of the rules beforehand.

Here are a few important considerations for AIA:

- For equipment to qualify, it’s not enough to buy it. It must be in use by the end of the year in which you claim the allowance and that includes assets bought on hire purchase. HMRC employ agents who know the difference between a cultivator and a combine, and can keep track of seasonal purchases.

- You must provide a purchase invoice to HMRC for any capital equipment, no matter how it is acquired. The date must fall within the period in which you’re claiming the allowance.

- If you’re an unincorporated partnership, you can’t claim AIA if one of the partners is a company or another partnership.

- A group of companies shares one AIA. The same applies where two or more businesses are controlled by the same person.

When you can claim

You can only claim AIA in the period you bought the asset. The date you bought the asset is:

- when you signed the contract if payment is due within 4 months.

- when payment’s due, if it’s due more than 4 months later.

1. Credit agreements (Hire Purchase)

Debt finance is a common way of buying capital equipment. When the agreement expires, ownership is transferred to the hirer. This type of credit agreement is called lease purchase or hire purchase, and counts towards your AIA (or writing-down allow-ance) in the same way as buying outright. Any interest you pay as part of the agreement counts as a business expense, so reduces your tax liability even further.

2. Hire agreements (Rental or Operating Lease)

Hire agreements involve a business simply hiring equipment for a period of time, and include Contract Hire, Operating Leases and Rental agreements. Once the agreement ends, you return the equipment. Rental payments count as a business expense, so they reduce pre-tax profits and the amount of tax you pay. HMRC works this out annually, based on the length of the lease.

3. Capital

You may choose to invest in business equipment using your cash reserves. If your business generates a return on cash that is higher than the interest charged on a lease or bank loan, you may find these alternatives to be more cost-effective. With the Office for National

Statistics (ONS) reporting an average of 12.5% return on capital for UK businesses, it’s highly likely that a return of that size will exceed interest charged when borrowing money.

Manitou Finance is not authorised to provide tax advice. You should consult an accountant in order to understand the tax consequences of any investment